Cancer Testing in 2026: The Four Pillars of Molecular Oncology

I stumbled onto OpenOnco a few weeks ago and couldn’t stop scrolling. It’s an open-source database created by Alex Dickinson that catalogs the molecular oncology testing landscape – 155 tests, 75 vendors, 6,743 trackable data points covering everything from turnaround times to FDA statuses to reimbursement codes. For someone like me – a software engineer who has spent time adjacent to bioinformatics but has never designed an assay – it was a goldmine. I could finally see the shape of an industry I’d been curious about for years.

I am not an assay scientist. Most of the domain context in this series comes from hours of research with the help of Claude and Gemini, cross-referenced against the OpenOnco dataset, published papers, and FDA filings. Think of this as a software person’s field guide to molecular oncology testing – what I found when I tried to make sense of the landscape, with all the caveats that implies.

This is the first post in a three-part series. Part 1 (this post) maps the four categories of cancer molecular testing and introduces the dataset. Part 2 dives into Minimal Residual Disease (MRD) – the fastest-moving category where a single test (Signatera) dominates reimbursement while 43 competitors fight for clinical evidence. Part 3 covers the early cancer detection wars – blood vs. stool, single-cancer vs. multi-cancer, and the FDA’s unprecedented approval streak in 2024.

Part 1: The Four Pillars (this post) | Part 2: MRD | Part 3: Screening Wars

The four pillars

Every molecular cancer test falls into one of four categories. They correspond to four questions a patient might ask across the cancer continuum.

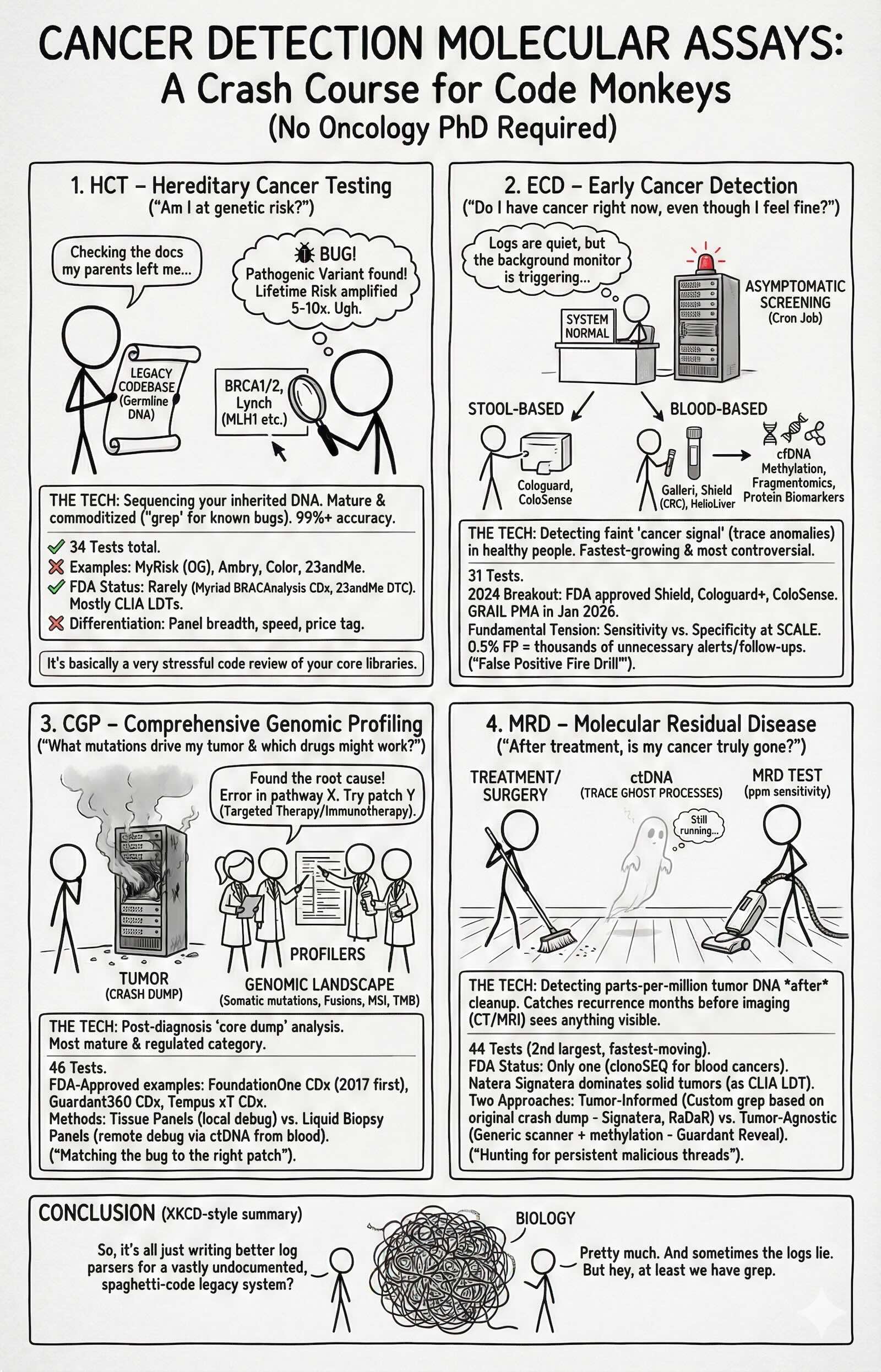

HCT – Hereditary Cancer Testing

“Am I at genetic risk for cancer?”

HCT tests sequence your germline DNA – the DNA you inherited from your parents – to look for pathogenic variants in genes like BRCA1, BRCA2, and the Lynch syndrome mismatch repair genes (MLH1, MSH2, MSH6, PMS2). If you carry one of these variants, your lifetime cancer risk can be 5-10x higher than average. There are 34 tests in this category, from Myriad’s MyRisk (the original) to newer panels from Ambry, Invitae/Labcorp, Color Health, and even 23andMe. Almost every one is a CLIA LDT. Only two have FDA clearance: Myriad’s BRACAnalysis CDx (a companion diagnostic for PARP inhibitors) and 23andMe’s DTC BRCA report. The technology is mature and commoditized – all of these tests cluster at 99%+ analytical sensitivity and specificity. The differentiation is in panel breadth, turnaround time, and price.

ECD – Early Cancer Detection

“Do I have cancer right now, even though I feel fine?”

ECD tests screen asymptomatic people for cancer. This is the most controversial and fastest-growing category. There are 31 tests here, split between stool-based colorectal screening (Cologuard, ColoSense) and blood-based approaches. The blood tests further divide into single-cancer screens (Shield for CRC, HelioLiver for HCC, FirstLook Lung) and multi-cancer early detection tests (Galleri, Shield MCD, OverC). The blood-based tests rely on cfDNA methylation patterns, fragmentomics, or protein biomarkers to detect cancer signal in people who have no symptoms. 2024 was a breakout year: the FDA approved Shield, Cologuard Plus, and ColoSense in rapid succession. GRAIL filed its PMA for Galleri in January 2026. The fundamental tension in this category is sensitivity vs. specificity at population scale – even a 0.5% false positive rate means thousands of unnecessary follow-ups when you screen millions of healthy people.

CGP – Comprehensive Genomic Profiling

“What mutations drive my tumor, and which drugs might work?”

CGP tests come after diagnosis. They profile the tumor’s genomic landscape – somatic mutations, fusions, amplifications, microsatellite instability, tumor mutational burden – to match patients with targeted therapies or immunotherapy. This is the most mature and most regulated category, with 46 tests. Foundation Medicine’s FoundationOne CDx was the first FDA-approved broad companion diagnostic (2017). Since then, Guardant360 CDx, Tempus xT CDx, MI Cancer Seek, TruSight Oncology Comprehensive, and several others have gained FDA approval or clearance. The category includes both tissue-based panels (FoundationOne CDx, MSK-IMPACT) and liquid biopsy panels (FoundationOne Liquid CDx, Guardant360 CDx) that profile circulating tumor DNA from a blood draw.

MRD – Molecular Residual Disease

“After treatment, is my cancer truly gone?”

MRD tests detect trace amounts of circulating tumor DNA (ctDNA) in the blood after surgery or treatment. The idea: if you can find tumor DNA fragments at parts-per-million concentrations, you can catch recurrence months before imaging (CT scans, MRI) would show anything visible. There are 44 tests in this category – the second-largest, and the fastest-moving. But only one has FDA clearance: Adaptive Biotechnologies’ clonoSEQ, which is cleared for blood cancers (multiple myeloma, ALL, CLL) – not solid tumors. Natera’s Signatera dominates the solid tumor MRD space as a CLIA LDT with ~70% commercial payer coverage. The category splits between tumor-informed approaches (Signatera, Haystack MRD, RaDaR) that require sequencing the original tumor to build a custom assay, and tumor-agnostic approaches (Guardant Reveal, Oncodetect) that use fixed panels plus methylation.

The patient journey

These four pillars map onto a patient’s trajectory through the cancer care continuum:

graph LR

A["Healthy Person"] --> B["Am I at risk?<br/><b>HCT</b>"]

B --> C["Do I have cancer?<br/><b>ECD</b>"]

C --> D["What drives it?<br/><b>CGP</b>"]

D --> E["Is it gone?<br/><b>MRD</b>"]

E --> F["Surveillance"]

F -.->|"recurrence?"| D

classDef default fill:none,stroke-width:2px

classDef hct fill:none,stroke:#fbbf24,stroke-width:2px

classDef ecd fill:none,stroke:#34d399,stroke-width:2px

classDef cgp fill:none,stroke:#a78bfa,stroke-width:2px

classDef mrd fill:none,stroke:#60a5fa,stroke-width:2px

classDef neutral fill:none,stroke:#9ca3af,stroke-width:2px

class A neutral

class B hct

class C ecd

class D cgp

class E mrd

class F neutral

Not every patient moves through all four stages. Someone with a BRCA2 variant (HCT) might get enhanced screening but never develop cancer. A patient diagnosed via conventional imaging skips ECD entirely. And MRD monitoring only applies after curative-intent treatment (surgery, chemo, radiation) – metastatic patients are typically managed with CGP-guided targeted therapy instead.

Key concepts

Before diving into the data, a few definitions that will recur throughout this series. These are simplified – if you’re an assay developer, you’ll find these reductive, but they’re good enough for the data exploration that follows.

cfDNA (cell-free DNA). When cells die – normal turnover, inflammation, or tumor cell death – they release fragments of their DNA into the bloodstream. These fragments are short (~160 base pairs) and get cleared within hours. Tumor-derived cfDNA (ctDNA) carries the mutations and methylation patterns of the cancer, which is what these tests detect. The challenge: ctDNA is a needle in a haystack, often less than 0.1% of total cfDNA in early-stage disease.

Sensitivity vs. Specificity. Sensitivity is the true positive rate – what fraction of actual cancers does the test catch? Specificity is the true negative rate – what fraction of cancer-free people get a clean result? Both matter, but they trade off. A test can achieve 100% sensitivity by calling everything positive, but specificity drops to zero. In population screening (ECD), specificity matters more than most people realize: screening 1 million people with a 99.5% specific test still generates 5,000 false positives.

CHIP (Clonal Hematopoiesis of Indeterminate Potential). As you age, some of your blood stem cells accumulate mutations and expand clonally – not cancer, but a pre-cancerous state. CHIP-associated mutations (DNMT3A, TET2, ASXL1) show up in cfDNA and can fool ctDNA-based tests into calling a false positive. This is the single biggest technical challenge for both MRD and ECD tests. Tumor-informed MRD assays sidestep CHIP by only tracking mutations known to come from the tumor. Tumor-agnostic assays must filter CHIP computationally, which is imperfect.

Tumor-informed vs. Tumor-agnostic. Two approaches to MRD testing. Tumor-informed assays (Signatera, Haystack MRD, RaDaR) start by sequencing the patient’s tumor and matched normal tissue, then build a custom PCR panel tracking 16-50 tumor-specific variants. This gives higher sensitivity (~0.001% tumor fraction) but requires tissue and takes 2-6 weeks to build. Tumor-agnostic assays (Guardant Reveal, Oncodetect) use a fixed gene panel plus methylation markers – no tissue needed, results in ~7 days, but generally lower sensitivity for small tumors.

LDT vs. FDA. An LDT (Lab Developed Test) is a test built and validated by a single CLIA-certified lab. No FDA review required – the lab self-validates under CLIA regulations. An FDA-approved test (PMA, 510(k), or De Novo) has undergone formal FDA analytical and clinical validation review. As of early 2026, the vast majority of cancer molecular tests are LDTs. The FDA finalized its rule to regulate LDTs in 2024, with a phased enforcement timeline starting in 2025 – this is reshaping the entire industry, as labs race to either submit for FDA approval or argue for exemptions.

The data

All of the analysis in this series is built on data from OpenOnco. It’s genuinely impressive work – someone (or a team) has methodically cataloged the entire molecular oncology testing landscape and made it open-source. The dataset covers 155 tests from 75 vendors across the four categories. There are 6,743 total data points tracked per test (clinical performance, regulatory status, reimbursement, sample requirements, turnaround time, etc.) with a 62% fill rate – meaning 4,202 fields have data. Data quality is tiered: Tier 1 data (sensitivity, specificity, regulatory status) has a 99% citation rate. About 20% of tests (31 out of 155) have vendor-verified data, where the test manufacturer reviewed and corrected OpenOnco’s entries.

The coverage is not uniform, which itself is interesting. CGP has the deepest data (longest-established category with the most FDA-approved tests). MRD has the most active changelog (fastest-moving category). ECD has the most contested data points (vendors actively disputing each other’s claimed performance). HCT has the shallowest data – the tests are commoditized and the vendors have little incentive to differentiate on published metrics.

The landscape at a glance

The treemap below shows every test in the dataset, grouped by category. Tile size is uniform – this is a map of the market’s breadth, not revenue. The number on each tile is the count of cancer types the test covers. Opacity indicates regulatory status: fully opaque tiles are FDA approved or cleared; translucent tiles are CLIA LDTs or earlier-stage. Hover for details on cancer types, sample requirements, and clinical performance.

The acceleration curve

New cancer tests are not launching at a steady rate. The chart below shows tests with identifiable launch or first-availability dates, stacked by category. The pattern is clear: CGP dominated 2017-2022, then MRD and ECD exploded starting in 2023.

100 tests had no identifiable launch year (including all 34 HCT tests).

What’s next

In Part 2: MRD, I dig into MRD – the fastest-moving category. I compare tumor-informed vs. tumor-agnostic approaches, look at the clinical evidence landscape, try to understand Signatera’s dominance (and its vulnerabilities), and visualize the sensitivity-vs-turnaround tradeoff across all 44 tests.

In Part 3: Screening Wars, I tackle the early cancer detection wars – blood vs. stool, single-cancer vs. multi-cancer screening, the FDA’s 2024 approval streak, and the population-scale math that makes specificity the most important number in medicine.

I’ve been having way too much fun with Gemini’s image generation lately – the xkcd-style hand-drawn look is irresistible for summarizing dense topics. Here’s my attempt at a one-page takeaway for this post.

TL;DR: 155 tests from 75 vendors now cover the full cancer timeline — risk, screening, profiling, and recurrence monitoring — but most are unregulated LDTs and the data is a mess.

TL;DR: 155 tests from 75 vendors now cover the full cancer timeline — risk, screening, profiling, and recurrence monitoring — but most are unregulated LDTs and the data is a mess.